Shaping Markets

Luxury Loopholes: Reforming the Illinois Tax Code

04. 22. 2026

A proposal to make Illinois millionaires pay state income tax on at least one-third of their income by closing luxury loopholes.

Executive Summary

The following memo analyzes changes to the calculation of taxable income to ensure tax filers who earn over $1 million annually pay the State’s flat income tax on a minimum of a third of their gross income. Estimates utilize FY22’s IDOR tax data (CY21).

Millionaire’s Minimum: Closing an Income Tax Loophole

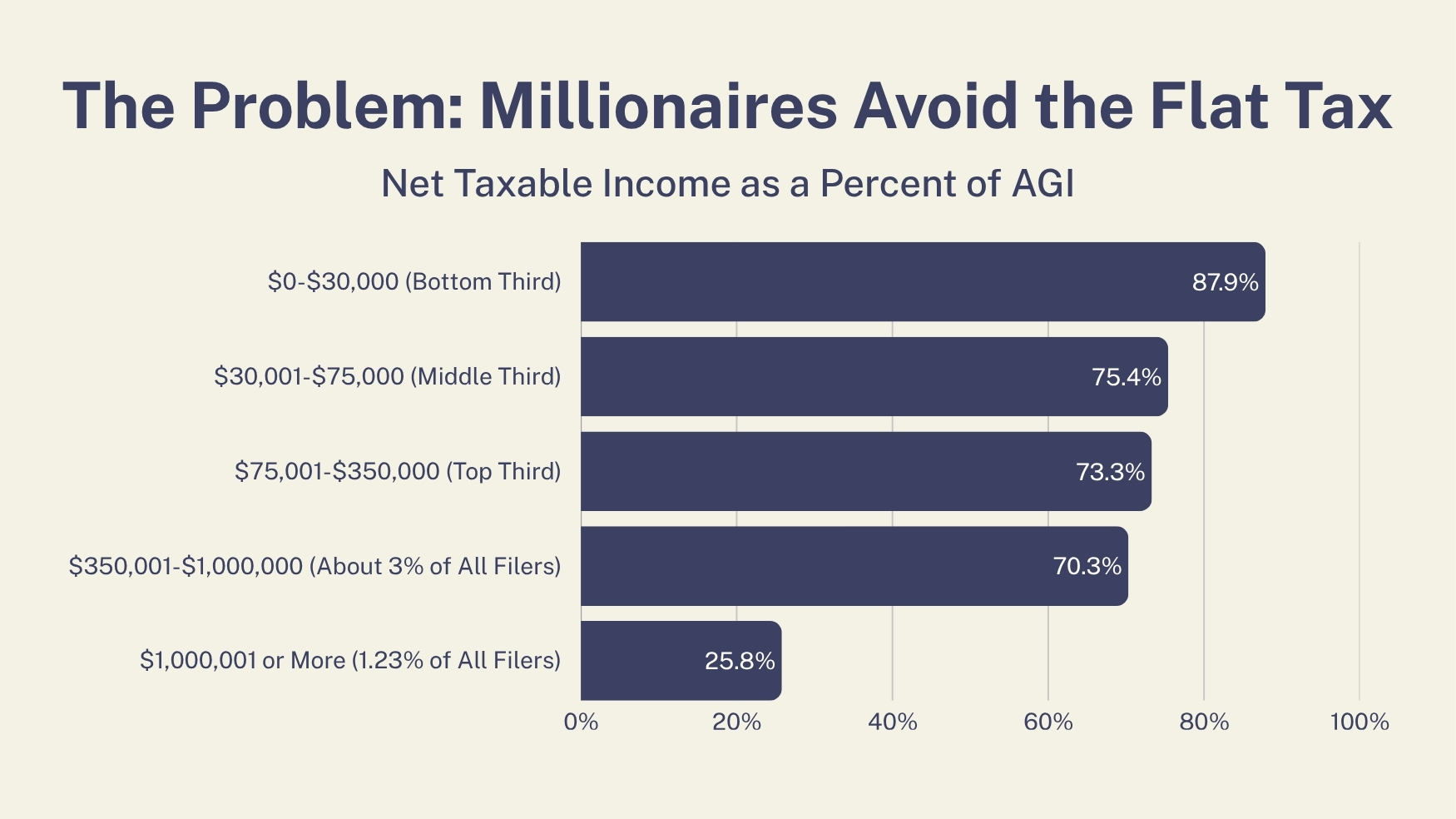

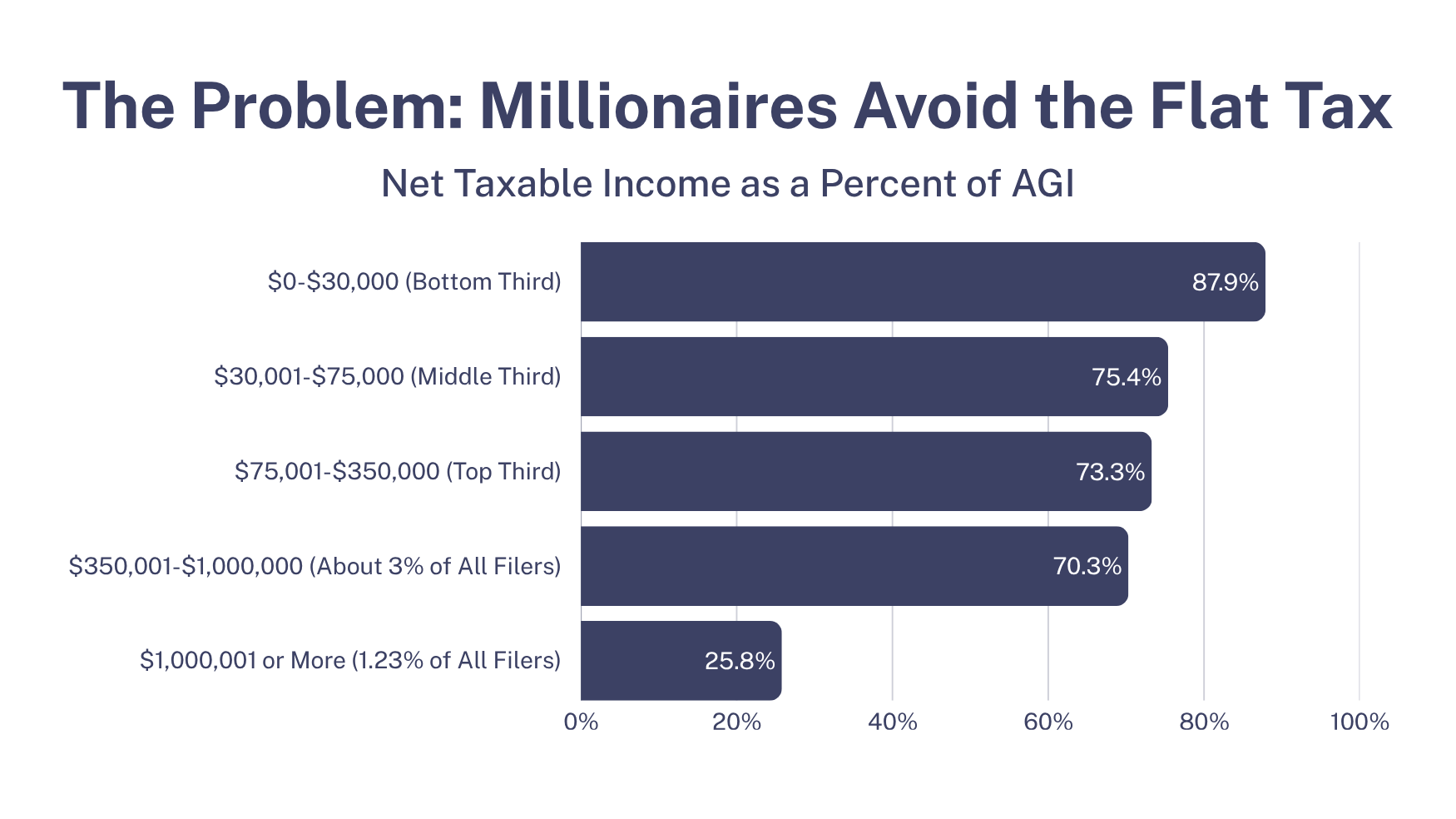

When calculating the amount of income to which Illinois’ personal income tax is applied for 98.77% of all filers, the ratio of taxable income to adjusted gross income (AGI) is about 70%. If we include the top 1.3% of earners – individuals who make over $1 million annually – the ratio drops from about 70% to 47%.

Individuals over $1 million AGI are paying State income tax on far less of their income than every other bracket. Individuals with $1M AGI collectively make up a total $626.3 billion in AGI, but have a taxable net income of $161.9 billion. At just 26% of their bracket’s AGI, millionaires’ average taxable income is a third less than all other filers in Illinois.

Setting a minimum net income to at least a third of base AGI for filers over $1 million would increase the taxable net income for millionaires alone, resulting in up to $2.32 billion in net new revenue. On average, this would result in an increase of taxable income by about 7% for millionaires. While some households may see a more substantial increase in their taxable income, Illinois could cap year-over-year increases. By doing so, the State maximizes revenue while smoothing year-over-year impact for outlier cases.

IDOR data is heavily stratified from $0 to $900,000 with some brackets containing as few as 9,000 filers. The publicly available dataset lacks stratification beyond $1M to analyze incomes over $1M. A more detailed look at the top 1.23% of earners (roughly 77,300 filers) would allow for a deeper review of impacts for those over $1M, $5M, and so on.

Calculation:

BASE AGI: $626,305,397,733

BASE NET INCOME: $161,887,926,689 (25.85%) = $8,013,458,717 (FY22’s net tax revenue)

NEW NET WITH CAP: $208,766,378,226 (33.33) = $10,333,935,722 (Gross tax revenue)

Subtract credits: – $167,159,713 (FY22’s tax credit amount)

Total Net Income Revenue: = $2,320,477,005

Source: Final 1040 IIT Return Files dated Oct. 2023 (FY22)

This calculation assumes no growth since FY22. Also, this estimate assumes all reported AGI is Illinois-based income. About 590,000 tax filers are out-of-state, and therefore only pay Illinois’ personal income tax on a portion of their income. Alternatively, Illinois-based residents may have out-of-state income that also wouldn’t be taxed by Illinois’ state income tax regardless of this proposal, but that income is reported in total AGI. Additional IDOR analysis is required to determine the full extent of both considerations’ impact on potential total revenue generation.

Structurally, we can accomplish this in one of two ways. Economic Security Illinois Action (ESILA) produced a legal memorandum highlighting the constitutionality of this proposal and presented it to IDOR in 2025. ESILA’s legal consultant is available to answer questions and design legislation at the request of the State. Two pathways for implementation considered in that memorandum to be viable are as follows:

- Set a broad requirement that a high-dollar earner’s net taxable income shall not be less than a third of their federal AGI (base income). This minimum requirement of 33% is scalable: ESILA has selected it as a placeholder. ESILA can run scenarios upon request.

- Alternatively, Illinois can cap individual deductions and credits available to high-dollar earners and disregard certain federal deductions to calculate federal AGI for state taxation purposes. To address tax disparity for high-dollar earners, an expanded scope with similar caps for all State deductions available to high-dollar earners, and cap (i.e., add back) federal deductions used to determine federal AGI for state taxation purposes. Some of these deductions could include business and real estate losses or pass-through deductions. Illinois already caps the availability of certain credits by income, for example:

- The property tax credit is limited to households making less than $500,000.

- The Earned Income Credit and Child Tax Credit are limited to federally structured income thresholds based on total dependents.

- The Educational Expense Credit is limited to households making less than $500,000

The memorandum reviewed both the flat tax requirement and the uniformity clause, successfully clearing potential challenges in ESILA’s review. In short, the memorandum found that Illinois’ Constitution restricts the State’s ability to levy multiple tax rates. However, the availability of credits, deductions, and other such “allowances” against one’s owed taxes are offered by the State of Illinois and are treated with broad discretion in the eyes of the courts. Limiting allowances are fully within the scope of the General Assembly, and ESILA’s view is that setting a minimum taxable income for Illinois by closing luxury loopholes brings our tax code closer to a true flat tax by applying the tax to more of a millionaire’s income.

ESILA’s legal memorandum is available upon request.