Affordability

Direct Cash to Help Californians Weather the Affordability Crisis

04. 22. 2026

Part of the 2026 Economic Security California Action Policy Agenda

Prices are high and rising: more than half of California renters spend more than 30% of their income on rent, and food prices are up 30% since 2019. But rising costs are only half the crisis. Wages haven’t kept pace, safety nets are being gutted, and too many Californians have no financial cushion when they experience unexpected hardship. Whether families can afford California depends as much on what’s in their bank accounts as what’s on the price tag. California has already done the hardest part: building the evidence and infrastructure that proves cash works. The state delivers more than $1.4 billion annually through refundable tax credits and pioneered the modern guaranteed income movement. What the state has already proven is that cash, delivered directly and reliably, gives people both the resources and agency to meet their needs and build the lives they want.

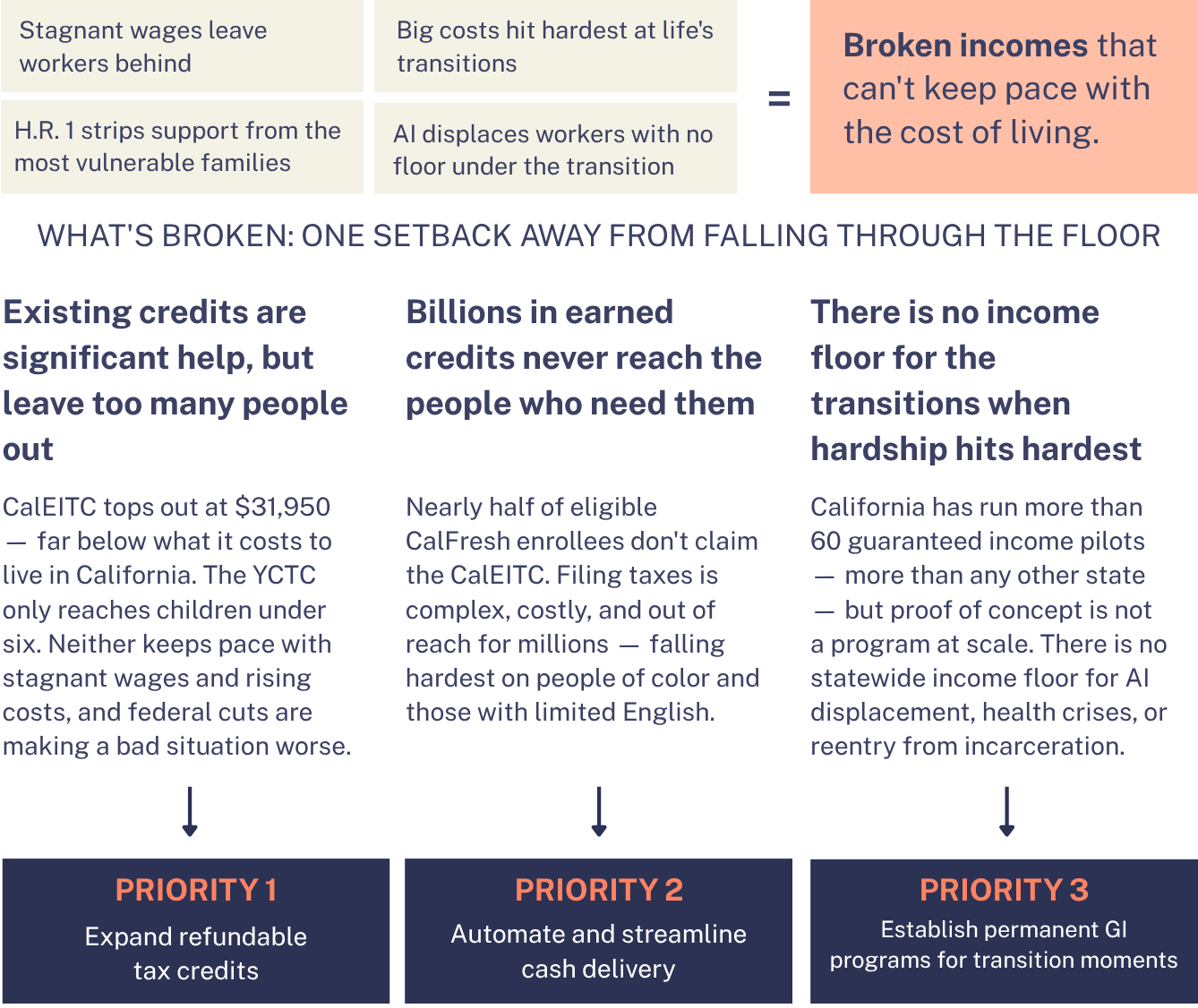

Broken Incomes: Rising costs leave too many Californians one setback away from falling through the floor

Low wages and eroding worker power mean, for many, one job is no longer enough. California has the world’s fourth-largest economy and the single largest influence on national productivity growth of any state. Our economy is powered by more than 19 million workers, 70% of whom work full-time. But the workers driving that prosperity aren’t sharing in it: 36% of California workers earn low wages (less than two-thirds the state median), and wages have grown just 2.9% after inflation since 2020 while the cost of living has kept climbing. That means having a job is far from a guarantee of economic security today. Among those who can’t afford basic needs, 80% live in working families, and 1.5 million California workers live in poverty. At the same time, the strength of worker power that once bridged the gap between wages and costs has eroded. California’s union membership hit a historic low of 14.5% in 2024, meaning millions of workers have been stripped of stable hours, benefits, and collective bargaining rights. When wages stagnate and worker power is diminished, cash creates the floor through which nobody can fall.

Big costs hit hardest during life transitions when income is lowest. The mismatch between life and earning cycles is a predictable feature of when and how people earn incomes and incur large costs over their lifetimes. Earnings usually climb with experience and peak in people’s forties and fifties, but the biggest expenses often hit much earlier or at unpredictable moments. The affordability crisis concentrates at transitions like the birth of a child, the purchase of a home, job loss or change, a health emergency, pursuing higher education, aging out of foster care, or reentry from incarceration. Costs are highest when income gaps are widest and safety nets are thinnest. The burden falls harder on many families of color: Black and Latinx families are significantly more likely to face economic insecurity and financial hardship than white Californians. Targeted cash at these moments prevents a temporary setback from becoming permanent poverty and can change life trajectories.

Federal cuts stripped support from the families most dependent on it. H.R. 1, passed in July 2025, delivered the largest cuts to Medicaid in history, cutting up to $30 billion a year from California, and gutted SNAP availability by instituting significant new barriers to eligibility. Both changes remove critical purchasing power from the households with the least margin for error. More people will fall into poverty: without safety net programs, California’s poverty rate would have been 6.7% higher in 2023. The damage H.R. 1 does to these programs will make families less economically resilient against the affordability crisis. Guaranteed income and expanded tax credits cannot replace the social safety net, nor fully supplement the cuts made to Medicaid and SNAP. What more cash could do is provide families with the liquid resources to absorb disruptions when those programs become unavailable. The H.R.1 cuts make the case for cash supports that families can count on regardless of what Washington does next.

AI displacement is already eroding income security, especially for early-career workers, and there’s no floor under the transition. A Stanford study of millions of payroll records found that employment for workers aged 22-25 in the most AI-exposed jobs (software development, customer service, accounting, and administrative work) has fallen 16% since ChatGPT launched, while older workers in the same roles saw employment grow. Companies are replacing the entry-level work that once built careers with AI, and not backfilling those roles. The workers most likely to be displaced are those with thin savings, specialized skills, and limited options where they live. Cash support in that transition gap gives workers the agency and time to land on their feet while new opportunities catch up. Building the capacity to distribute cash in acute moments of need now is how California can get ahead of the displacement rather than scramble to respond to it.

The Affordability Agenda: California has proven cash is a powerful economic stabilizer

In both ordinary economic conditions and unprecedented crises, California has demonstrated that well-designed cash policies are effective and popular, helping families cover essentials, prevent financial crises, and make choices that help them live their lives with stability and agency. Because it allows people to spend how they need to, the support is tailored to each person’s specific circumstances: paying off a credit card bill, being present at the big moments in their children’s lives, not having to take a second (or third) job. Cash is not a silver bullet. It cannot solve deeply broken markets, such as the lack of affordable childcare or inaccessible healthcare, which require sustained public investment and policy reforms to truly meet families’ needs. But it can still play a critical role in helping families stabilize in the short term while broader structural reforms are pursued. Research consistently shows that the most pronounced positive impacts occur when cash is delivered at critical life transitions: welcoming a new child, going to school, navigating a career transition, reentering the workforce after incarceration, or after a traumatic event. The question is no longer whether cash works, but how we can build on its proven success.

What’s Working: A Nation-Leading Cash Delivery System

California has built some of the country’s strongest state tax credits for low-income families. Refundable tax credits are among the most effective antipoverty tools available for working-age families. These credits are proven to outperform other safety net programs on long-run poverty reduction, employment, and reduced reliance on public assistance, while putting cash directly in people’s hands with relatively low administrative burden. Our state version of the Earned Income Tax Credit, the CalEITC, was created in 2015 and has been expanded repeatedly since to increase income eligibility, extend to immigrant filers with ITINs (Individual Taxpayer Identification Numbers), and add two new credits: the Young Child Tax Credit (YCTC) in 2019 and the Foster Youth Tax Credit (FYTC) in 2022. In 2022, the state eliminated the income requirement for the YCTC so that families with zero earnings could still qualify. Together, these three credits now deliver over $1.4 billion annually to nearly 6 million Californians, reaching workers, families with young children, and former foster youth transitioning into adulthood.

When the COVID recession hit, California proved not only that emergency cash works, but that the state can deploy it to quickly reach people at risk of being left behind. At its peak, the pandemic recession pushed unemployment to 20% or higher for workers of color in California, leaving millions unable to work and exhausting whatever savings they had. The largest state tax rebate in American history, the Golden State Stimulus, delivered $12 billion in direct payments to low-income Californians automatically, through the existing tax filing system, with no separate application required. Crucially, it included ITIN filers, reaching undocumented families who were explicitly shut out of federal stimulus. That was a deliberate policy choice, and a significant one in a state where more than half of all workers are immigrants or children of immigrants.

California pioneered the modern guaranteed income movement, and the evidence it generated has reshaped what’s possible. In 2019, Economic Security Project partnered with then-Mayor Michael Tubbs on the Stockton Economic Empowerment Demonstration (SEED), the first mayor-led GI demonstration in the country, which gave 125 randomly selected participants $500 a month for two years. SEED participants were more likely to find full-time work, experienced more stable incomes, and reported better mental health outcomes. That proof of concept seeded a movement: California now has more than 60 GI programs statewide, far more than any other state. Nationally, guaranteed income programs have reached more than 200 pilots supporting 50,000 participants, with more than 12,000 in California. The state took the next step in 2021, when the Legislature established the first-ever state-funded guaranteed income program: a $35 million, five-year CDSS program providing $600 to $1,200 per month to nearly 2,000 Californians, focused on pregnant individuals and foster youth aging out of care.

What’s Broken: Current Programs Are Not Adequate, Fully Inclusive

The credits and programs California has built still leave too many people out. CalEITC excludes the lowest-income workers from the full credit. This gap is an artifact of the phase-in structure inherited from the federal EITC. The credit tops out at incomes of $31,950, far below what it actually costs to live in most of California, where more than 1 in 3 households can’t afford basic needs even with working adults. Moreover, most recipients receive less than $200. The YCTC reaches only families with children under six. Neither keeps pace with what workers actually face: stagnant wages, eroding union power, and rising living costs. Federal cuts are making a bad situation worse: as H.R. 1 strips purchasing power from households with the least margin for error, state credits should increase to cushion the fallout. California can’t offset a $30 billion Medicaid cut with a $1.4 billion tax credit program. The state needs to significantly expand what it delivers and who it reaches.

Billions of dollars in earned credits never make it to the people who need it. Nearly half of eligible CalFresh enrollees didn’t claim the CalEITC, because claiming it requires filing taxes. Not only is filing taxes not required for the lowest-income Californians, but when they do, it is complex and often expensive. The time tax (hours spent navigating fragmented bureaucratic systems) falls hardest on low-income families, people with limited English, and those without internet access. Critically, this policy failure is a racial equity failure: 79% of Californians eligible for the CalEITC and 84% of those eligible for the YCTC are people of color, and people of color have been shown to be more than twice as likely as white families to miss out on benefits delivered through the tax code. Too many families are locked out by a filing process that’s too complex, too costly, and too inaccessible for families already stretched too thin. As the federal government retreats from Direct File, the window for efficiently and free of charge getting tax credits to people is getting smaller, not bigger.

There is no income floor for the transitions when hardship hits hardest. California has run more than 60 guaranteed income programs, more than any other state. Evidence shows direct, unconditional cash improves health outcomes, stabilizes finances, and gives participants more agency over their lives. Yet, proof of concept is not a program at scale. There is no statewide income floor for a worker displaced by AI, or for someone who has to quit work to deal with a health crisis of their own or a family member’s. These transitions are predictable, and they’re becoming more common. California should act to make cash available at these critical moments, before people fall through the gap.

What’s Needed: More Cash, Delivered Reliably

California’s affordability crisis would be ameliorated by smart cash policies. The following three priorities would expand what the state delivers, fix the systems failing to deliver it, and create the income floor that many Californians need but don’t yet have.

PRIORITY 1: Expand Refundable Tax Credits

Every dollar invested in refundable tax credits goes directly into household budgets, and California’s infrastructure to deliver them is already built. The state should increase credit amounts, broaden income eligibility, establish a minimum credit to end the exclusion of the lowest-income households, and extend the YCTC beyond children under six. With H.R. 1 stripping critical support from the households with the least margin for error, expanding credits now is both good policy and one of the fastest and most effective ways California can deliver help to the families that need it.

PRIORITY 2: Automate and Streamline Tax Credit Delivery

Millions of Californians who qualify for tax credits never claim them, but the state has much of the information needed to help them do it with much less burden. The state can reach eligible families in multiple ways: strategically sharing data it already holds across agencies like EDD and CDSS to identify non-filers; meeting people where they already interact with government (enrolling in benefits, recertifying for programs, or visiting state offices) and using those touchpoints to capture the tax information needed to deliver credits automatically; and building proactive outreach into the filing system itself. Concretely: (1) the Franchise Tax Board (FTB) should automatically issue refunds for unclaimed credits where eligibility can be confirmed from existing data; (2) the state should build a year-round tool for gig workers and independent contractors to track earnings, manage estimated payments, and access refundable tax credits; and (3) the FTB should reengage lapsed filers with pre-filled prior-year returns. As the federal government retreats from Direct File, California can’t afford to wait.