Affordability

Corporate Tax Fairness to Fund a More Affordable California

04. 22. 2026

Part of the 2026 Economic Security California Action Policy Agenda

Affordability is the defining issue in California today. The Golden State’s economy is among the largest in the world, but the gains of its prosperity bypass the millions of Californians who are responsible for its success. While wages stagnate, the cost of basics continues to climb: food prices are up 30% since 2019, electricity prices are 80% higher than the national average, and 82% of California households cannot afford to buy a median-priced home. The revenue required for shared prosperity should come from the corporations whose market power is driving the affordability crisis. California has the tools to make them pay for it. Closing corporate tax loopholes, holding large firms accountable as employers, and modernizing a tax structure that advantages multinationals over small businesses would generate billions in sustainable revenue and fund the investments Californians need.

Broken Budget: Federal Cuts Worsened an Already Buckling Fiscal Foundation

California’s budget crisis is structural and deepening. While the Governor’s proposed 2026–27 budget identifies a $2.9 billion shortfall, the Legislative Analyst’s Office estimates an $18 billion shortfall for 2026–27, with continuing large deficits of $35 billion in 2027–28 and beyond. This year is the fourth consecutive year of deficits despite strong revenue growth, driven by AI-fueled stock market gains that the LAO warns are unsustainable. If the stock market corrects, revenues could collapse.

The state has already exhausted most of its budget reserves addressing prior shortfalls, leaving California with fewer tools than ever to respond. The state carries $33.9 billion in outstanding budgetary borrowing, has depleted the Safety Net Reserve, and the Governor’s proposed $248.3 billion General Fund includes no significant new revenue measures.

The federal cuts from H.R. 1 could turn a strained situation into a catastrophe. H.R. 1, passed in July 2025, delivers the largest cuts to Medicaid in history. It strips up to $30 billion in annual federal Medicaid funding from California and puts 3.4 million Californians at risk of losing coverage. These costs will shift onto an already strained state budget, forcing lawmakers to choose between cutting care and cutting everything else, unless the state generates new revenue. At the same time, the expiration of Affordable Care Act (ACA) premium subsidies is pushing premiums up by an average of $975 a year for 1.5 million Covered California enrollees, and a projected 660,000 Californians will lose health coverage altogether. For families already stretched by housing, energy, and childcare costs, losing healthcare coverage compounds the affordability squeeze on every family.

The Affordability Agenda: When Corporations Pay Their Share, California Can Invest in Everyone

California’s tax code has significant strengths but a structural failure at its core. Currently, a robust graduated personal income tax funds the public investments and refundable tax credits that support Californians. However, over the last four decades, large corporations have reduced their tax liability through loopholes and lower rates, while simultaneously using their concentrated wealth and market power to drive up the costs of housing, healthcare, energy, and childcare. These corporations inflate costs with market power and starve the state’s response through tax avoidance, and Californians pay twice.

What’s Working: A Progressive Foundation for Families

California’s personal income tax is one of the most progressive in the nation, with a separate bracket for millionaires that tops out at 13.3%. Counting income, sales, excise, and property taxes, Californians across income groups pay roughly the same share of their income in taxes. That progressive revenue base funds refundable tax credits that deliver cash directly to Californians. This amounts to over $1.4 billion annually through CalEITC, the Young Child Tax Credit, and the Foster Youth Tax Credit, collectively reaching millions of Californians each year. ESCA’s work has been central to building this infrastructure by tripling the CalEITC, establishing the Young Child Tax Credit, and expanding both credits to ITIN filers.

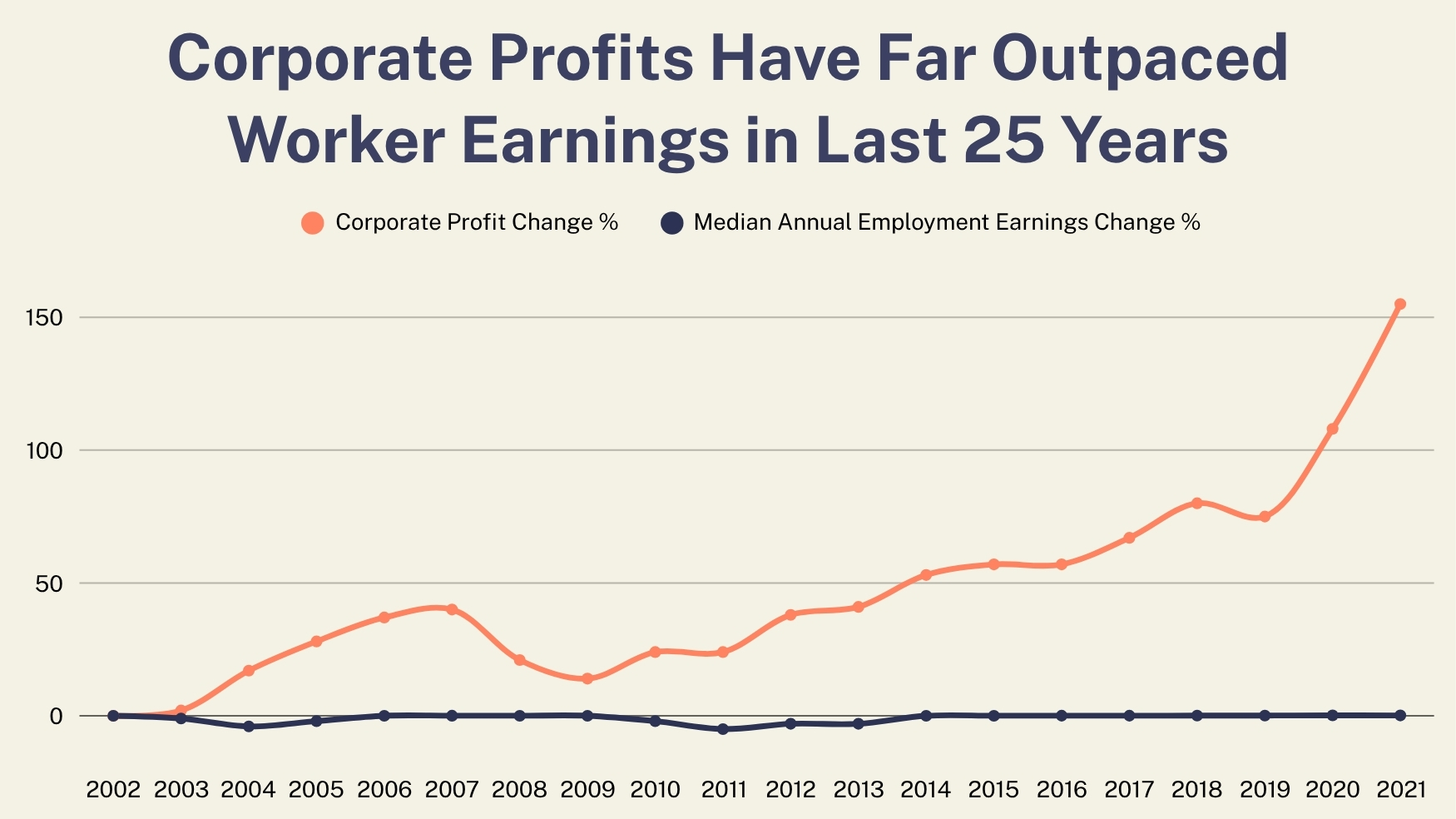

What’s Broken: The Corporations Driving the Affordability Crisis Are Starving the State’s Response

Source: California Budget & Policy Center Analysis of Franchise Tax Board and US Census Bureau, Current Population Survey via IPUMS

California corporations are paying a shrinking share of their profits to the state, even as those profits continue to climb. Today, corporations pay roughly half the share of their profits in state taxes that they paid in the 1980s. California’s flat corporate tax charges a small business earning $50,000 and a multinational earning $50 billion the same rate, while giving the multinational a set of loopholes the small business cannot use. The corporations exploiting those loopholes are the same ones using market power to drive up costs for families, and every dollar lost to corporate tax avoidance is a dollar unavailable to lower housing costs, expand healthcare coverage, and put cash in the pockets of hardworking Californians.

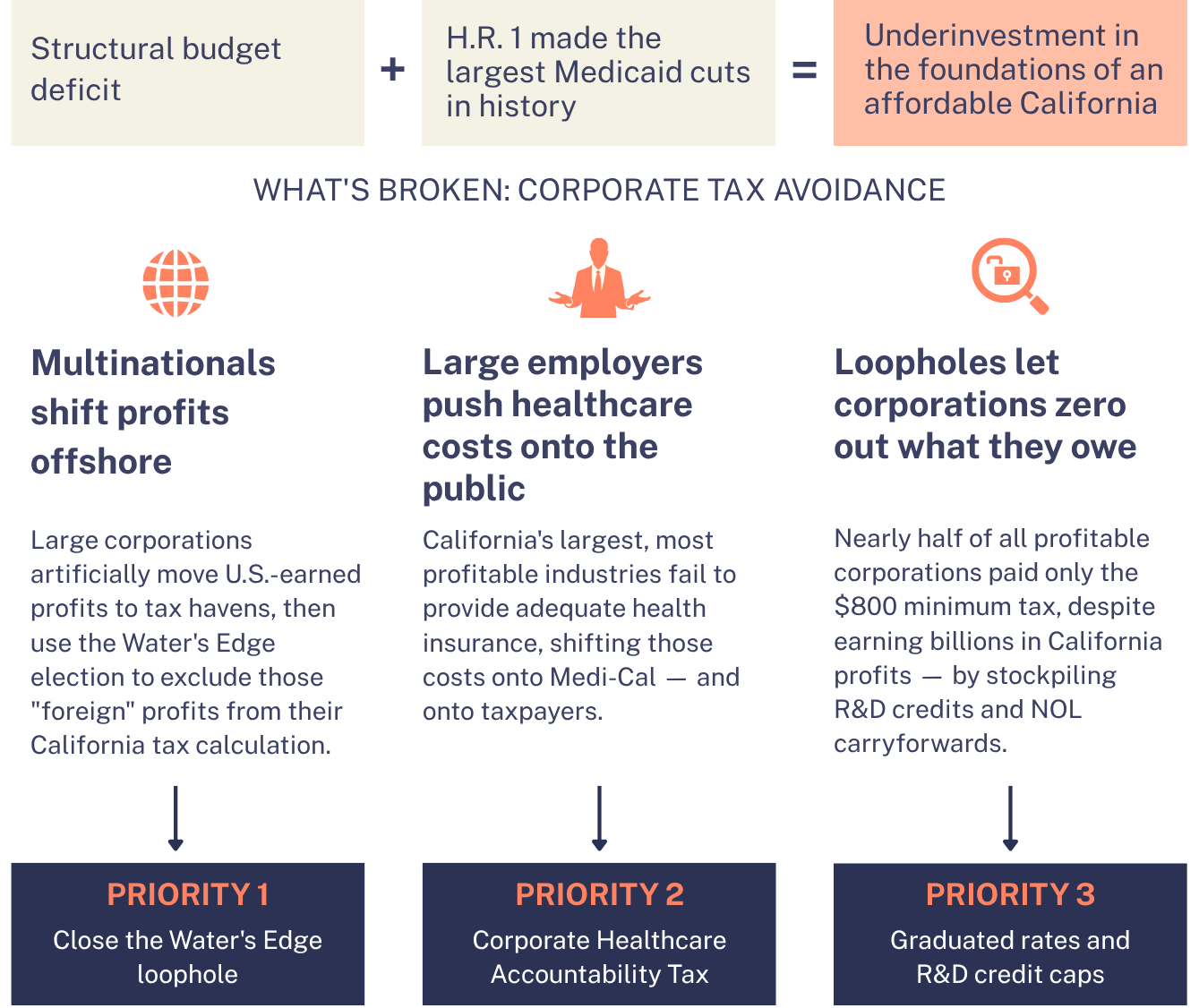

Multinationals shift profits offshore to avoid California taxes. Large corporations with foreign subsidiaries can artificially move U.S.-earned profits to tax havens, then use the Water’s Edge election to exclude those “foreign” profits from their California tax calculation. This loophole costs the state $3.5 billion in revenue each year while giving multinationals a tax advantage otherwise unavailable to California’s 4.2 million small businesses.

Large employers push healthcare costs onto the public. Some of California’s largest and most profitable industries, including agriculture, food services, and retail, fail to provide adequate health insurance to their workers, instead shifting those costs onto Medi-Cal. A 2024 national survey of warehouse workers at Amazon, one of California’s largest private employers, found that nearly half relied on public assistance, including 20% who were relying on Medicaid. In other multistate surveys, Walmart and McDonald’s top the lists of companies with the largest numbers of employees enrolled in Medicaid. At a time when millions of Californians face premium increases and coverage losses, the state is subsidizing corporations that can afford to cover their own workers but choose not to. When the state pays for what should be an employer’s responsibility, those costs are shifted onto taxpayers.

Unlimited credits and deductions let large corporations zero out what they owe. Nearly half of all profitable corporations paid only the $800 minimum tax in 2023, despite collectively earning $11.7 billion in profits in California. The state spends $2.5 billion a year on the R&D tax credit, with no rigorous evaluation of whether it works. The largest beneficiaries have stockpiled credits to cut their state tax bills for years: Alphabet holds $6.4 billion in California R&D credits, Apple holds $3.5 billion, and pharmaceutical companies use the same credit to make minor modifications to existing medications and block generic competition. None of these tax advantages has come back in the form of revenue.

What’s Needed: Corporate Tax Reforms To Fund California’s Affordability Response

The mechanisms driving this crisis have clear fixes. The following three reforms would generate billions in sustainable revenue and directly target the corporate tax avoidance starving California’s response.

PRIORITY 1: Close the Water’s Edge Loophole

California already has the legal and administrative infrastructure to eliminate this loophole. The state taxes corporations using worldwide combined reporting when they do not elect the Water’s Edge method, requiring them to include all profits, domestic and foreign, before calculating what share is taxable to California. Closing the loophole would make that the default for all corporations with foreign parents or subsidiaries, ending the ability to cherry-pick which profits count. The U.S. Supreme Court has twice upheld the constitutionality and fairness of worldwide combined reporting as a method of taxing multinational corporations.

Closing the Water’s Edge loophole would level the playing field for small businesses. The Water’s Edge loophole is structurally available only to multinationals with foreign subsidiaries. California’s 4.2 million small businesses have no equivalent option. Every dollar those small businesses pay in taxes that a multinational avoids is a competitive disadvantage built into the tax code itself. Closing the loophole would raise revenue while also making our business environment more competitive for small businesses and startups.

PRIORITY 2: Corporate Healthcare Accountability Tax

Corporations that do not cover their workers should pay into the system on which they rely. Under this proposal, corporations that do not provide adequate health insurance to their employees would pay a tax penalty that funds California’s healthcare programs and offsets federal cuts to Medi-Cal.

This tax directly targets the broken markets driving up healthcare costs for Californians. The same dominant employers driving down wages and pricing workers out of private coverage are the ones pushing the highest costs onto the public budget. The Corporate Healthcare Accountability Tax ensures that corporations that shirk their responsibility to employees cannot offload healthcare costs to the state.

PRIORITY 3: Graduated Corporate Tax Rates & R&D Reform

Replacing California’s flat corporate tax rate with a graduated structure would lower costs for small businesses, and capping unlimited credits would end large corporations’ ability to zero out their tax liability. Pairing the graduated structure with caps on R&D credits and Net Operating Loss (NOL) carryforwards would close the domestic avoidance gap that Water’s Edge reform alone does not address. Corporations currently apply NOLs from prior years to erase current profits, then carry forward R&D credits indefinitely to eliminate any remaining liability. Reasonable annual caps on both would end the practice of zeroing out state tax bills entirely.

These reforms level the playing field for small businesses while ensuring large corporations contribute to the public investments that make their California operations possible. The effective tax rate of the largest 10% of corporations is already 11 to 16 percentage points lower than that of the remaining 90%. This gap reflects not the statutory rate but the capacity of the largest corporations to exploit it. A graduated rate combined with reasonable caps on R&D credits for large corporations would narrow that gap, restore fair competition for small businesses, and generate sustainable revenue to fund housing, healthcare, and economic supports for all Californians.